Code

library(tree)

library(ISLR2)All the code here is derived from the legendary book ISRL 2nd edition’s chapter 8 “Decision Trees”. Its sometimes a wonder how elegant the base R language can be. The ISRL lab rarely mentions tidyverse syntax but yet manages to make the code so easy to read. The more you learn!🤓

library(tree)

library(ISLR2)In today’s lab, we will be using the Carseats dataset from the ISLR2 package.

str(Carseats)'data.frame': 400 obs. of 11 variables:

$ Sales : num 9.5 11.22 10.06 7.4 4.15 ...

$ CompPrice : num 138 111 113 117 141 124 115 136 132 132 ...

$ Income : num 73 48 35 100 64 113 105 81 110 113 ...

$ Advertising: num 11 16 10 4 3 13 0 15 0 0 ...

$ Population : num 276 260 269 466 340 501 45 425 108 131 ...

$ Price : num 120 83 80 97 128 72 108 120 124 124 ...

$ ShelveLoc : Factor w/ 3 levels "Bad","Good","Medium": 1 2 3 3 1 1 3 2 3 3 ...

$ Age : num 42 65 59 55 38 78 71 67 76 76 ...

$ Education : num 17 10 12 14 13 16 15 10 10 17 ...

$ Urban : Factor w/ 2 levels "No","Yes": 2 2 2 2 2 1 2 2 1 1 ...

$ US : Factor w/ 2 levels "No","Yes": 2 2 2 2 1 2 1 2 1 2 ...Creating a column called High which takes a Y/N value depending on the sales and then merge it with the Carseats df.

attach(Carseats)

High <- factor(ifelse(Sales <= 8, "No", "Yes"))

Carseats <- data.frame(Carseats, High)CarseatsCreating a classification tree to predict High using all variables except Sales

set.seed(1)

tree.carseats <- tree(High ~ .-Sales, data = Carseats)

summary(tree.carseats)

Classification tree:

tree(formula = High ~ . - Sales, data = Carseats)

Variables actually used in tree construction:

[1] "ShelveLoc" "Price" "Income" "CompPrice" "Population"

[6] "Advertising" "Age" "US"

Number of terminal nodes: 27

Residual mean deviance: 0.4575 = 170.7 / 373

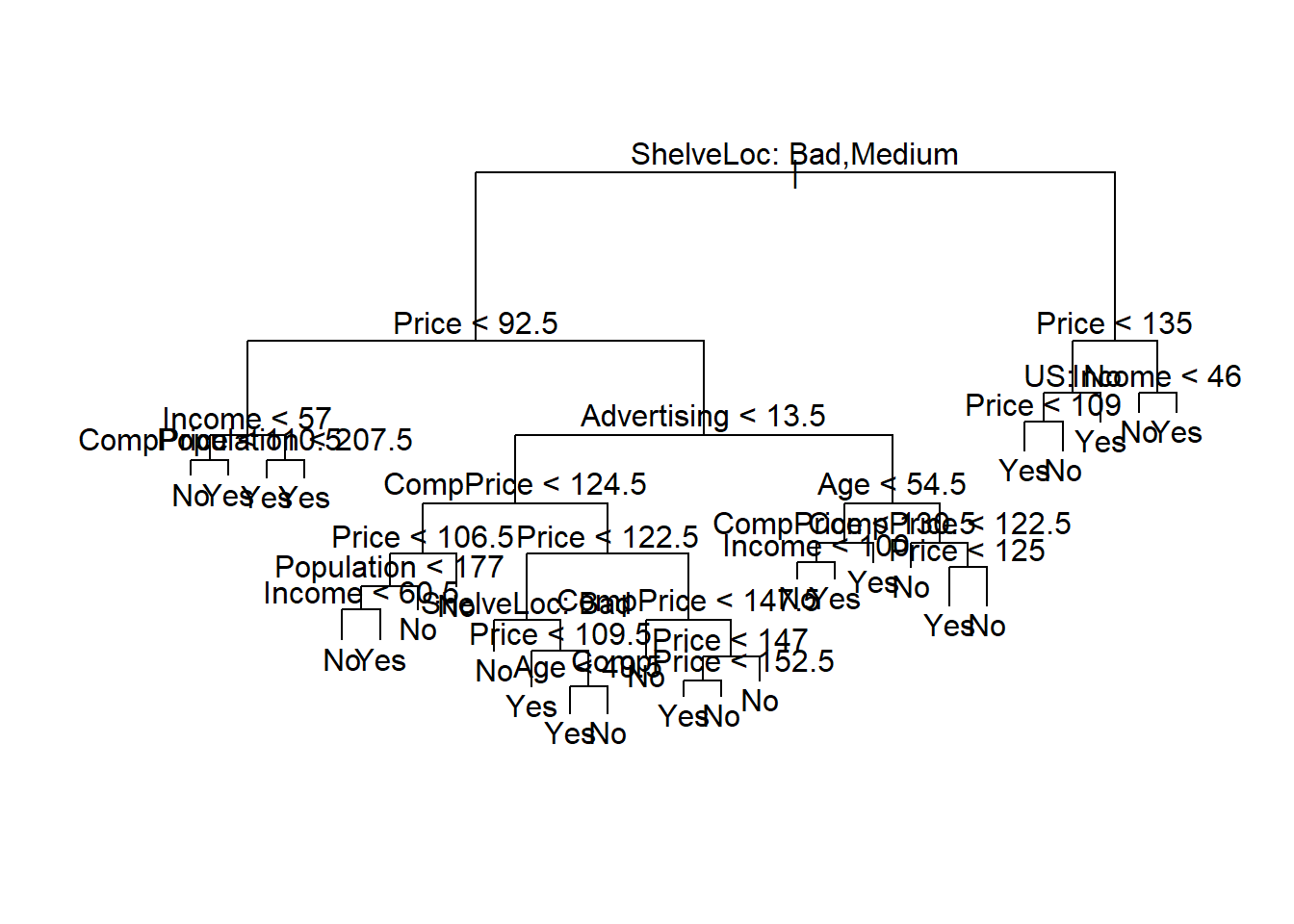

Misclassification error rate: 0.09 = 36 / 400 Misclassification error of 9% is a good fit. Let’s try plotting it

plot(tree.carseats)

text(tree.carseats, pretty =0 )

set.seed(2)

train <- sample(1:nrow(Carseats), 200)

Carseats.test <- Carseats[-train,]

High.test <- High[-train]

tree.carseats <- tree(High ~ .-Sales, data = Carseats,

subset = train)checking the top few rows of predicted columns

tree.predict <- predict(tree.carseats, Carseats.test,

type = "class") #type is needed to declare classification model

head(tree.predict)[1] Yes No No Yes No No

Levels: No YesComparing predicted with actual values

table(tree.predict, High.test) High.test

tree.predict No Yes

No 104 33

Yes 13 50What’s the accuracy?

(104+50)/200[1] 0.7777% Accuracy

To improve the accuracy, lets attempt to prune the tree. For this cv.tree() function is used to determine the optimal level of tree complexity. Here the FUN argument is taken as prune.misclass to indicate that the cross-validation and tree pruning should be guided by the classification error instead of the default deviance.

set.seed(7)

cv.carseats <- cv.tree(tree.carseats, FUN = prune.misclass)

names(cv.carseats)[1] "size" "dev" "k" "method"Note to self:

k is the regularisation parameter \(\alpha\) (alpha)size is # of terminal nodes for each treedev is the number of cross-validation errorscv.carseats$size

[1] 21 19 14 9 8 5 3 2 1

$dev

[1] 75 75 75 74 82 83 83 85 82

$k

[1] -Inf 0.0 1.0 1.4 2.0 3.0 4.0 9.0 18.0

$method

[1] "misclass"

attr(,"class")

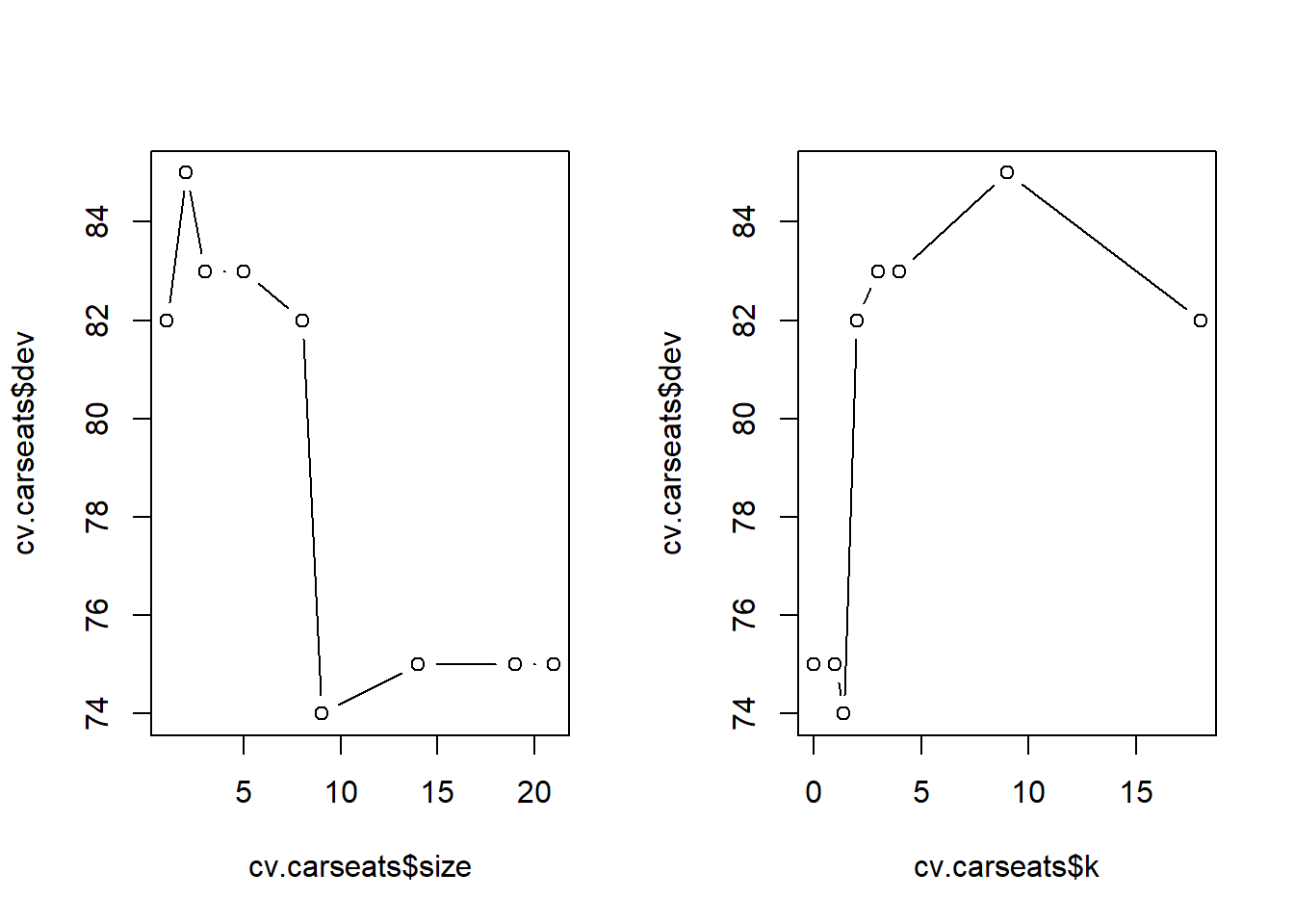

[1] "prune" "tree.sequence"Visualising the tree. The classification error is least (74) at size = 9

par(mfrow = c(1,2))

plot(cv.carseats$size, cv.carseats$dev, type = "b")

plot(cv.carseats$k, cv.carseats$dev, type = "b")

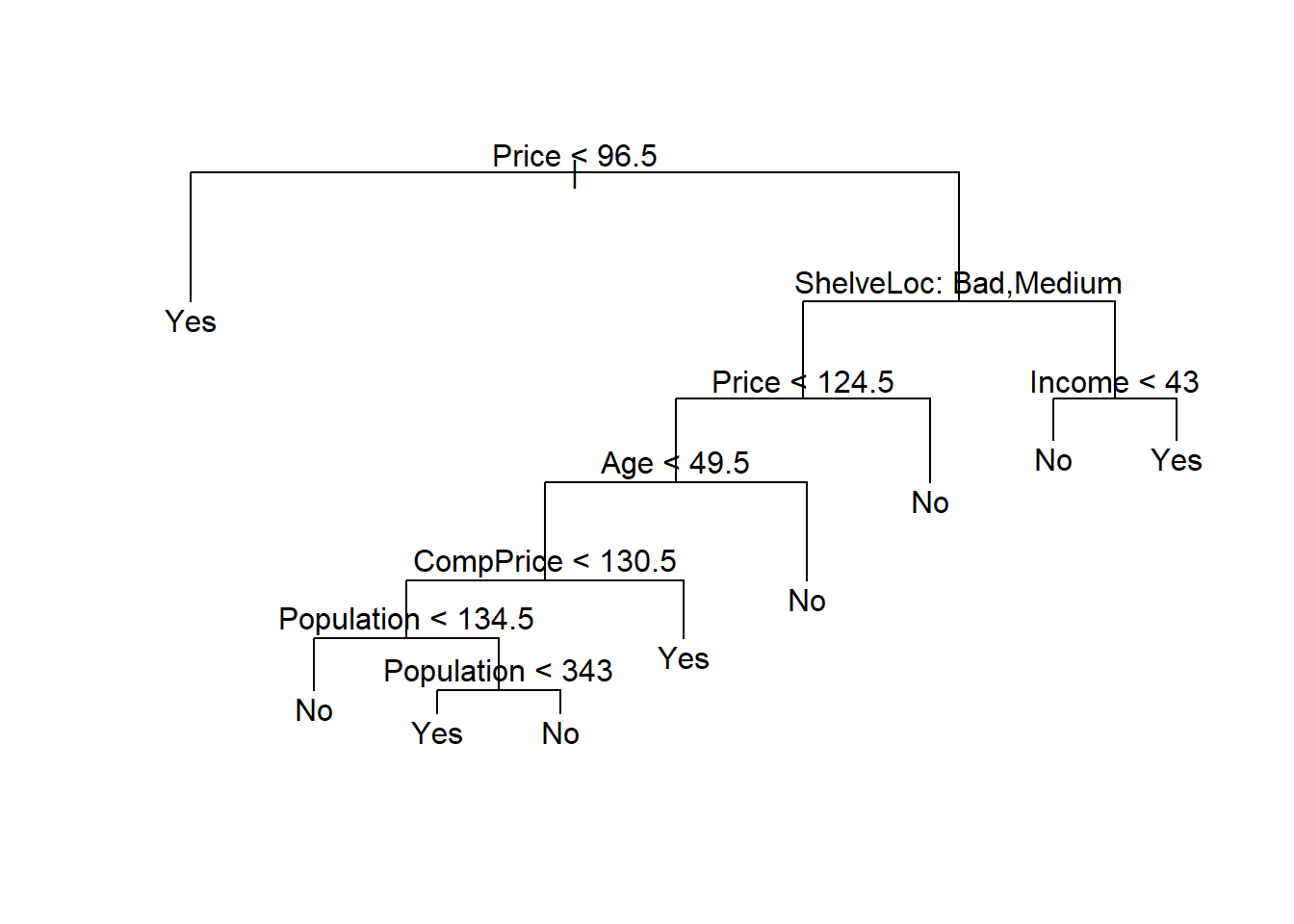

Using the prune.misclass() function to prune the tree to the 9-node specification.

prune.carseats= prune.misclass(tree.carseats, best = 9)

plot(prune.carseats)

text(prune.carseats, pretty = 0)

Checking the accuracy in the good-old fashioned way (its really that simple!)🤓

prune.tree.pred <- predict(prune.carseats, Carseats.test, type = "class")

table(prune.tree.pred, High.test) High.test

prune.tree.pred No Yes

No 97 25

Yes 20 58So what’s the accuracy?

(97+58)/200[1] 0.77577.5% which is slightly better than the non-pruned tree. Not bad.

tidymodels interface allows for managing the resulting output and models in a more structured way.Boston datasetBoston dataset contains housing values of 506 suburbs of Boston. We are trying to predict the median value of the owner-occupied homes medv

str(Boston)'data.frame': 506 obs. of 13 variables:

$ crim : num 0.00632 0.02731 0.02729 0.03237 0.06905 ...

$ zn : num 18 0 0 0 0 0 12.5 12.5 12.5 12.5 ...

$ indus : num 2.31 7.07 7.07 2.18 2.18 2.18 7.87 7.87 7.87 7.87 ...

$ chas : int 0 0 0 0 0 0 0 0 0 0 ...

$ nox : num 0.538 0.469 0.469 0.458 0.458 0.458 0.524 0.524 0.524 0.524 ...

$ rm : num 6.58 6.42 7.18 7 7.15 ...

$ age : num 65.2 78.9 61.1 45.8 54.2 58.7 66.6 96.1 100 85.9 ...

$ dis : num 4.09 4.97 4.97 6.06 6.06 ...

$ rad : int 1 2 2 3 3 3 5 5 5 5 ...

$ tax : num 296 242 242 222 222 222 311 311 311 311 ...

$ ptratio: num 15.3 17.8 17.8 18.7 18.7 18.7 15.2 15.2 15.2 15.2 ...

$ lstat : num 4.98 9.14 4.03 2.94 5.33 ...

$ medv : num 24 21.6 34.7 33.4 36.2 28.7 22.9 27.1 16.5 18.9 ...Creating the training set for Boston which is half the size of the original

set.seed(1)

train.boston <- sample(1:nrow(Boston), nrow(Boston)/2)Building the tree

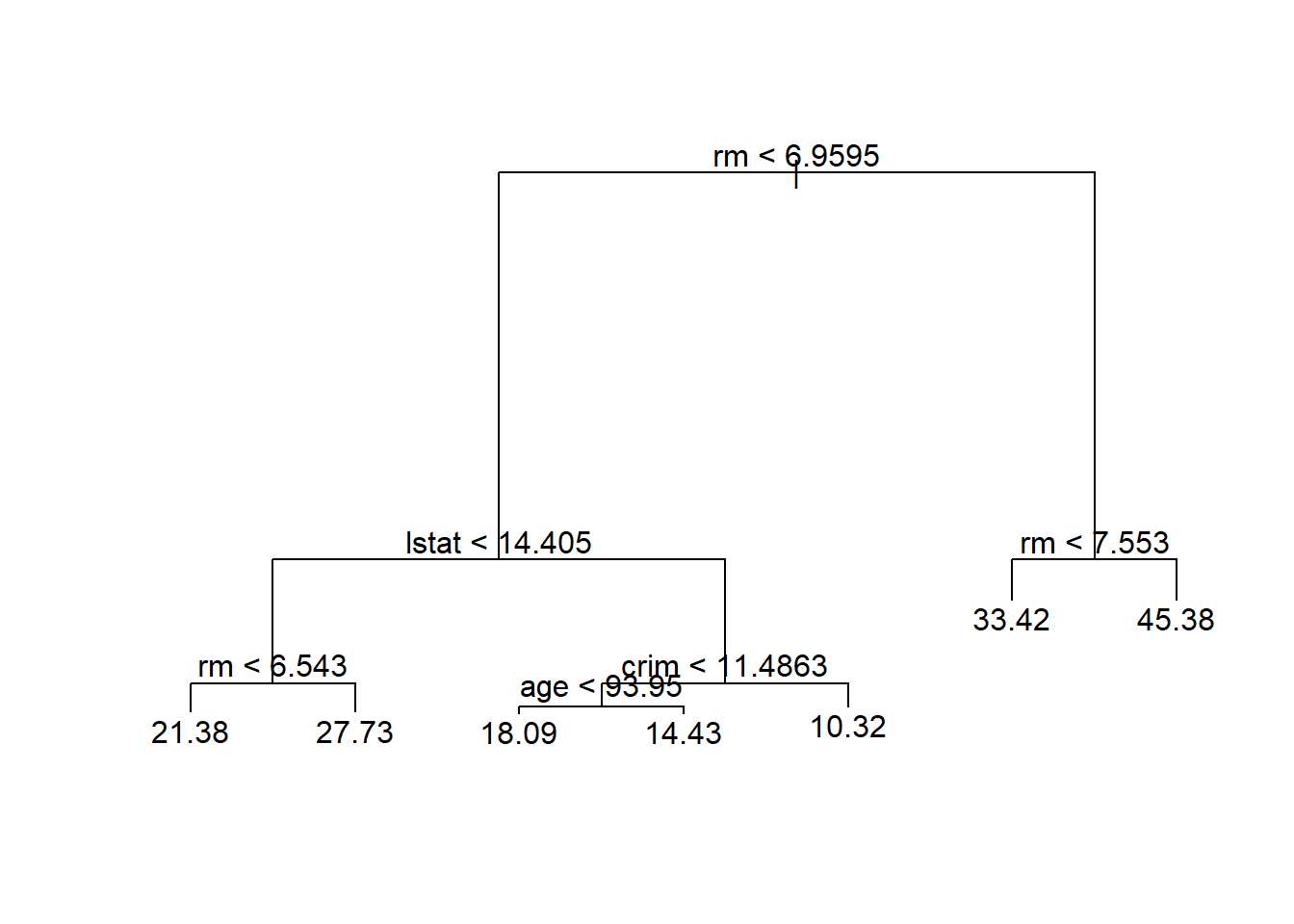

tree.boston <- tree(medv ~ ., data = Boston, subset = train.boston)

summary(tree.boston)

Regression tree:

tree(formula = medv ~ ., data = Boston, subset = train.boston)

Variables actually used in tree construction:

[1] "rm" "lstat" "crim" "age"

Number of terminal nodes: 7

Residual mean deviance: 10.38 = 2555 / 246

Distribution of residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-10.1800 -1.7770 -0.1775 0.0000 1.9230 16.5800 only 4 predictors rm, lstat, crim, age were used. (wonder why?) Plotting the decision tree

plot(tree.boston)

text(tree.boston, pretty = 0)

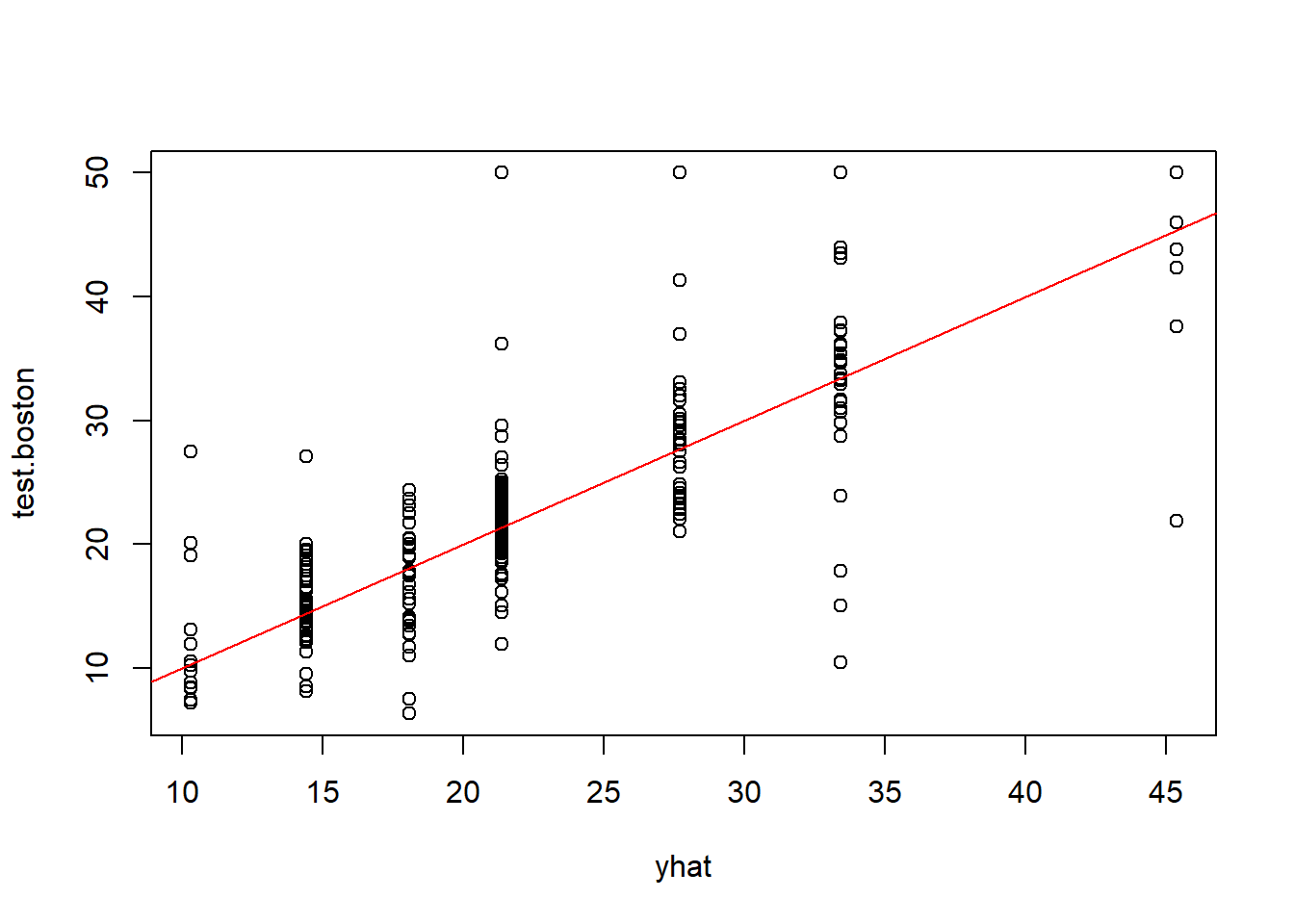

yhat <- predict(tree.boston, newdata = Boston[-train.boston,])

test.boston <- Boston[-train.boston,"medv"]

plot(yhat, test.boston)

abline(0,1, col = "red")

Mean Square Error is defined as \[MSE = \frac{1}{n} \sum_{i=1}^{n}(y_i - \hat{y_i})^2\]

mean((yhat - test.boston)^2)[1] 35.28688RMSE which uses the same units as the output variable is:

(mean((yhat - test.boston)^2))^0.5[1] 5.940276As the SD is the same units as the outcome variable, we can say that this model leads to predictions which on an average are within ±$5940 of the true median home value. Can we do better? Let’s keep digging

Note: Bagging is a special case of Random Forest where \(m = p\). The randomForest() function can be used for evaluating predictions from both bagging & RF. So first up is the Bagging process

\(m\) = sample number of predictors

\(p\) = total number of available predictors

importance parameter here will compute and return the importance measures of each predictor variable. Importance measures provide a way to assess the relative importance of each predictor variable in the random forest model, based on the decrease in accuracy that occurs when that variable is excluded from the model. This increases the runtime significantly on large datasets

library(randomForest)

set.seed(1)

bag.boston <- randomForest(medv ~ . , data = Boston,

subset = train.boston,

mtry = 12, # m = p

importance = T)

bag.boston

Call:

randomForest(formula = medv ~ ., data = Boston, mtry = 12, importance = T, subset = train.boston)

Type of random forest: regression

Number of trees: 500

No. of variables tried at each split: 12

Mean of squared residuals: 11.40162

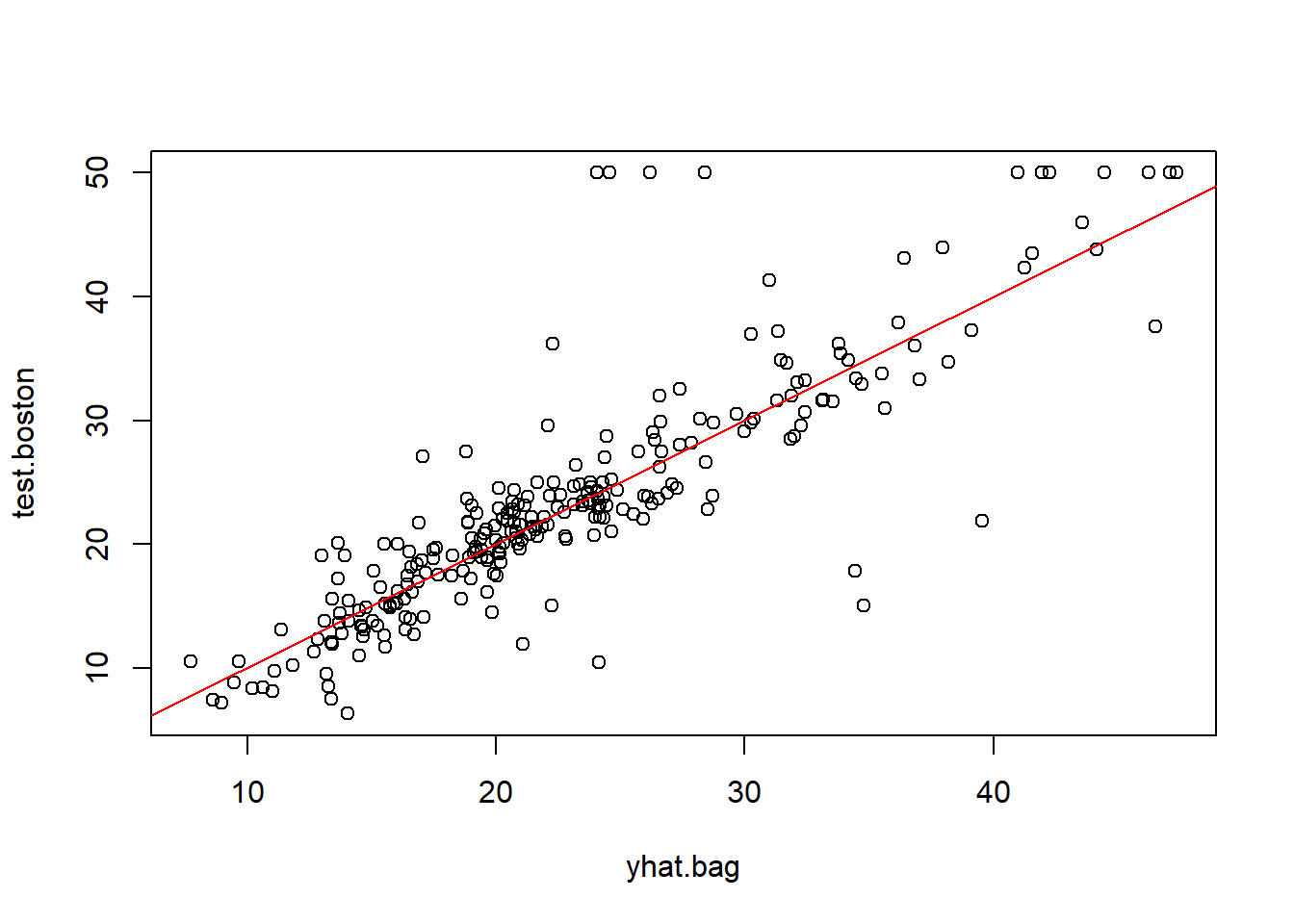

% Var explained: 85.17yhat.bag <- predict(bag.boston, newdata = Boston[-train.boston, ])

plot(yhat.bag, test.boston)

abline(0,1,col = "red")

What’s the accuracy here? Checking the MSE

mean((yhat.bag - test.boston)^2)[1] 23.41916And square root of MSE or RMSE is:

(mean((yhat.bag - test.boston)^2))^0.5[1] 4.839335That’s $4839 which is better than $ 5940 derived from the 7-node decision tree discussed in Key Takeaways. Moving to Random Forest now.

Its the same code, but we alter the number of predicted variables to \(m= 6\) which is the mtry parameter

Default settings for randomForest()

for regression analysis, \(m = p/3\)

for classification analysis, \(m = \sqrt p\)

set.seed(1)

rf.boston <- randomForest(medv ~ . , data = Boston,

subset = train.boston,

mtry = 6, # m = p/2

importance = T)

rf.boston

Call:

randomForest(formula = medv ~ ., data = Boston, mtry = 6, importance = T, subset = train.boston)

Type of random forest: regression

Number of trees: 500

No. of variables tried at each split: 6

Mean of squared residuals: 10.09466

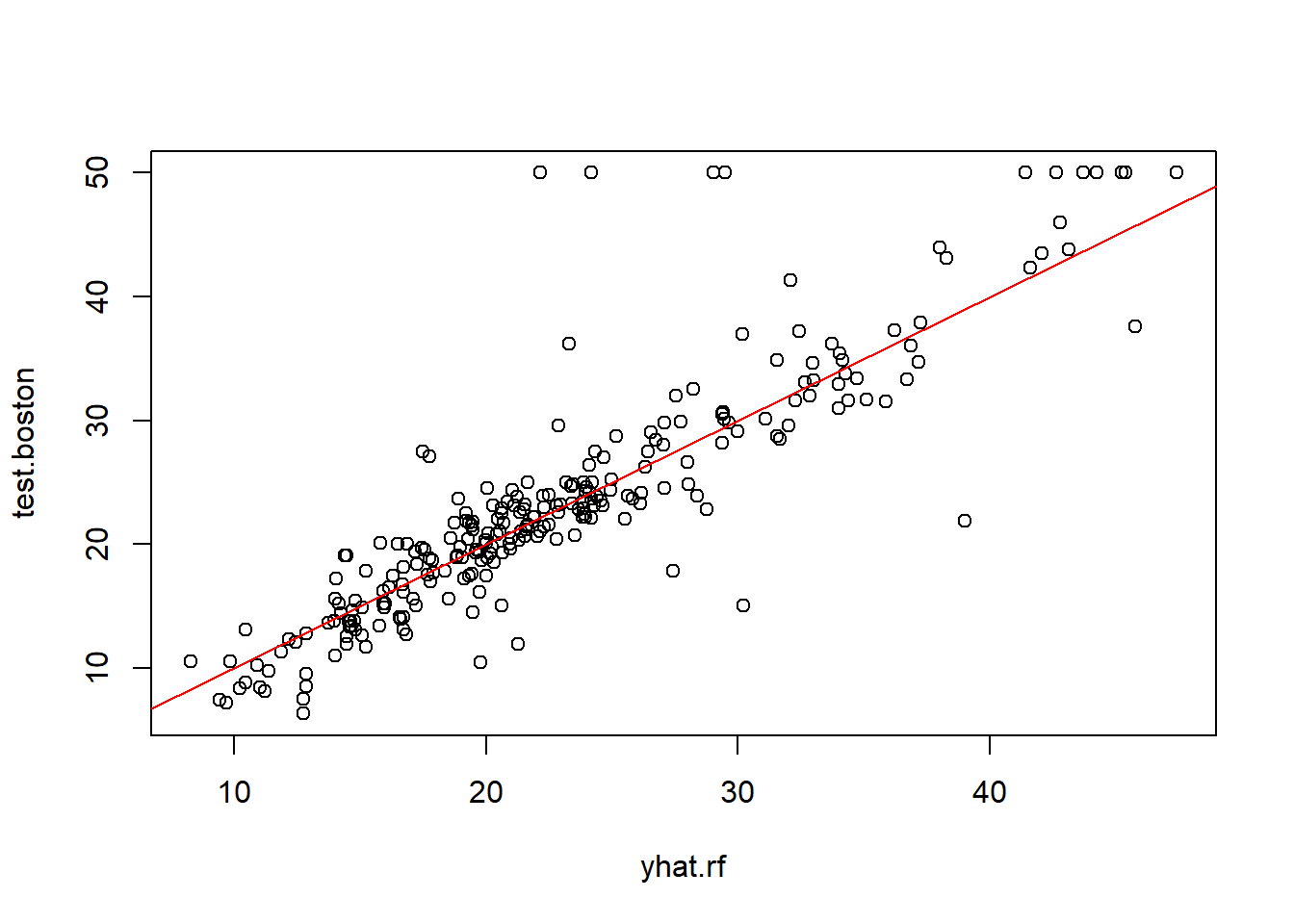

% Var explained: 86.87yhat.rf <- predict(rf.boston, newdata = Boston[-train.boston, ])

plot(yhat.rf, test.boston)

abline(0,1,col = "red")

What’s the MSE here?

mean((yhat.rf - test.boston)^2)[1] 20.06644.. and therefore RMSE is:

mean((yhat.rf - test.boston)^2)^0.5[1] 4.479558That’s ±$4480 from the mean predicted values - which is better than $4839 by using the Bagging method.

Before moving ahead, we can also check the importance() function to determine key predictors

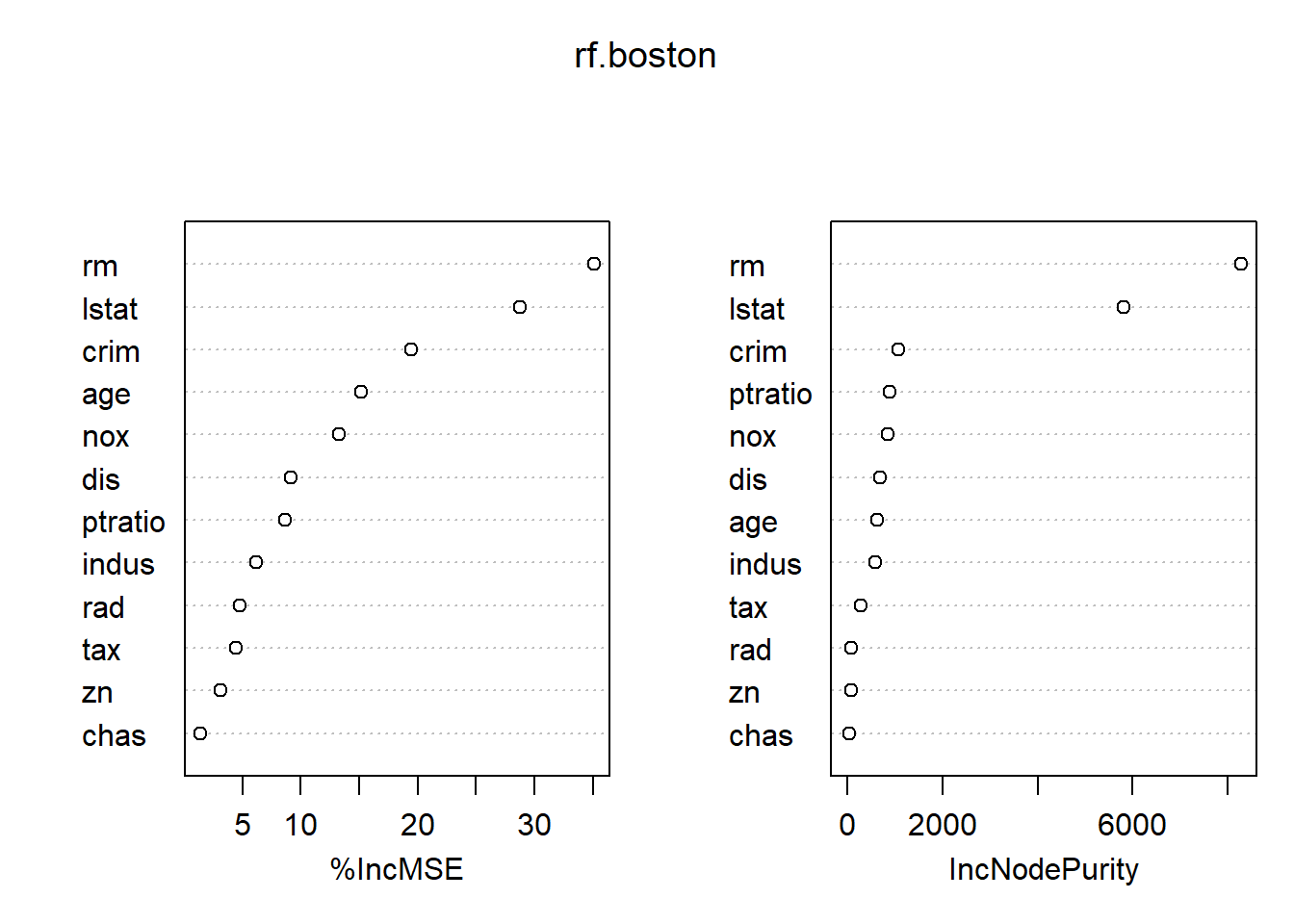

importance(rf.boston) %IncMSE IncNodePurity

crim 19.435587 1070.42307

zn 3.091630 82.19257

indus 6.140529 590.09536

chas 1.370310 36.70356

nox 13.263466 859.97091

rm 35.094741 8270.33906

age 15.144821 634.31220

dis 9.163776 684.87953

rad 4.793720 83.18719

tax 4.410714 292.20949

ptratio 8.612780 902.20190

lstat 28.725343 5813.04833What are these columns?

in regression trees, the node impurity measured by the training Residual Sum of Squares(RSS)

in classification trees, it is the deviance

varImpPlot(rf.boston)

This shows that the two most important variables are rm (average number of rooms per dwelling) and lstat (lower status of the population in %)

Using the gbm package (Gradient Boosting Model) for boosted trees. Few notes:

distribution = "gaussian" is considered for regression trees. For classification, it should be distribution = "bernoulli"n.trees = 5000 is the number of trees we want to iterate overinteraction.depth = 4 limits the depth of each treelibrary(gbm) #Gradient Boosting Models

set.seed(1)

boost.boston <- gbm(medv ~ ., data = Boston[train,],

distribution = "gaussian",

n.trees = 5000,

interaction.depth = 4)

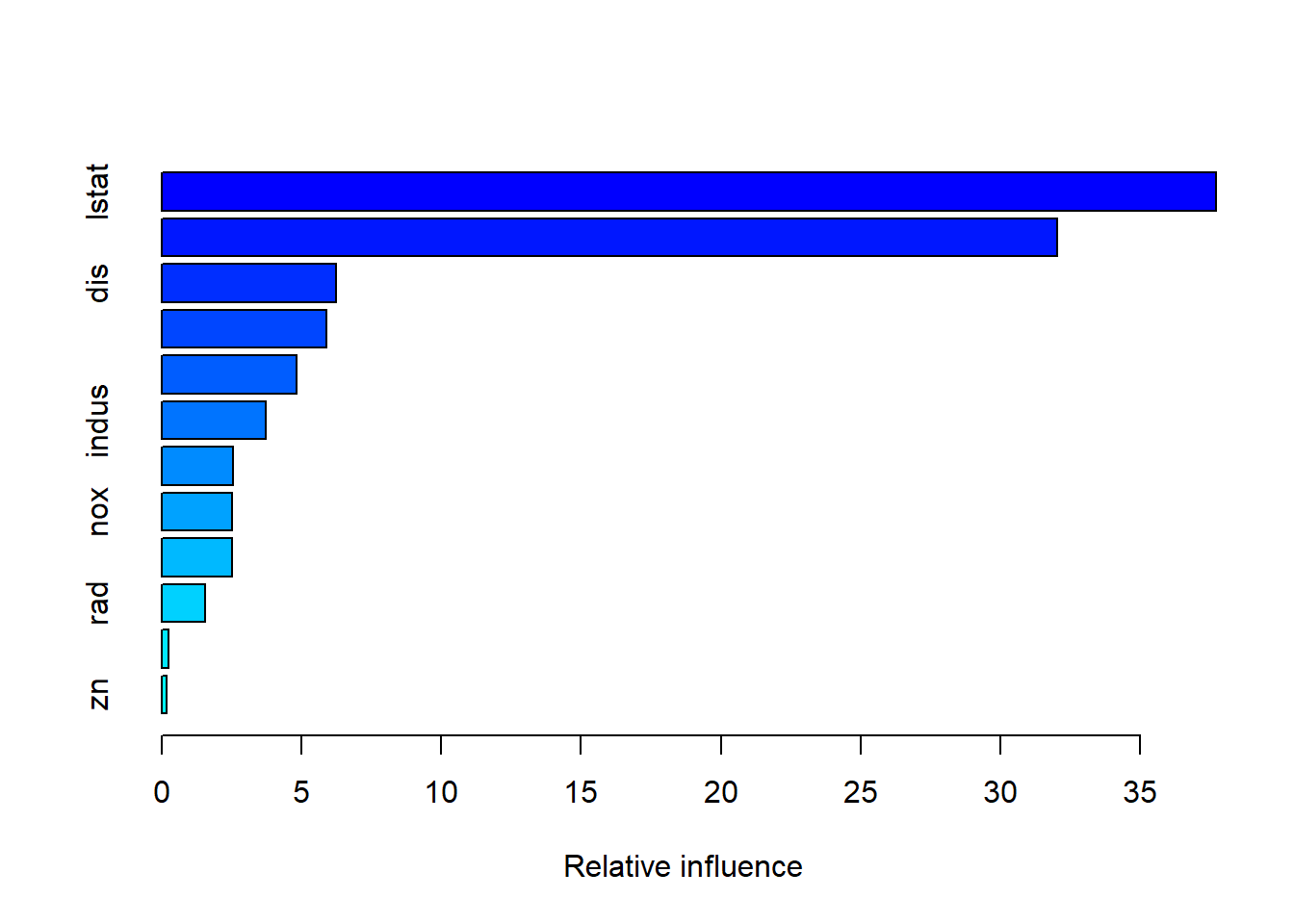

summary(boost.boston)

var rel.inf

lstat lstat 37.7145639

rm rm 32.0396810

dis dis 6.2532723

crim crim 5.9078403

age age 4.8163355

indus indus 3.7365846

tax tax 2.5457121

nox nox 2.5286998

ptratio ptratio 2.5091014

rad rad 1.5427771

chas chas 0.2451445

zn zn 0.1602876As seen earlier, lm and rstat show up as the most important variables.

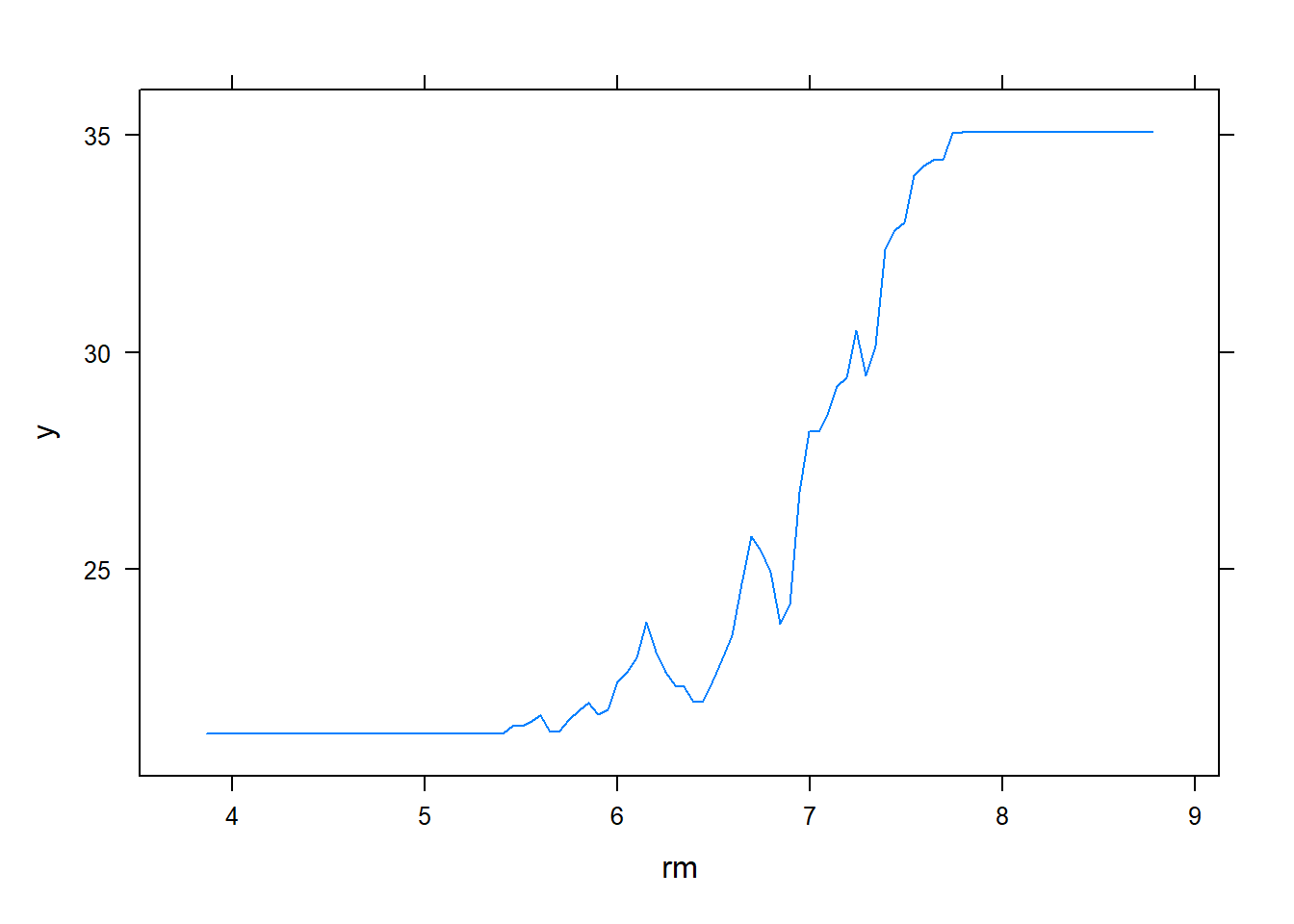

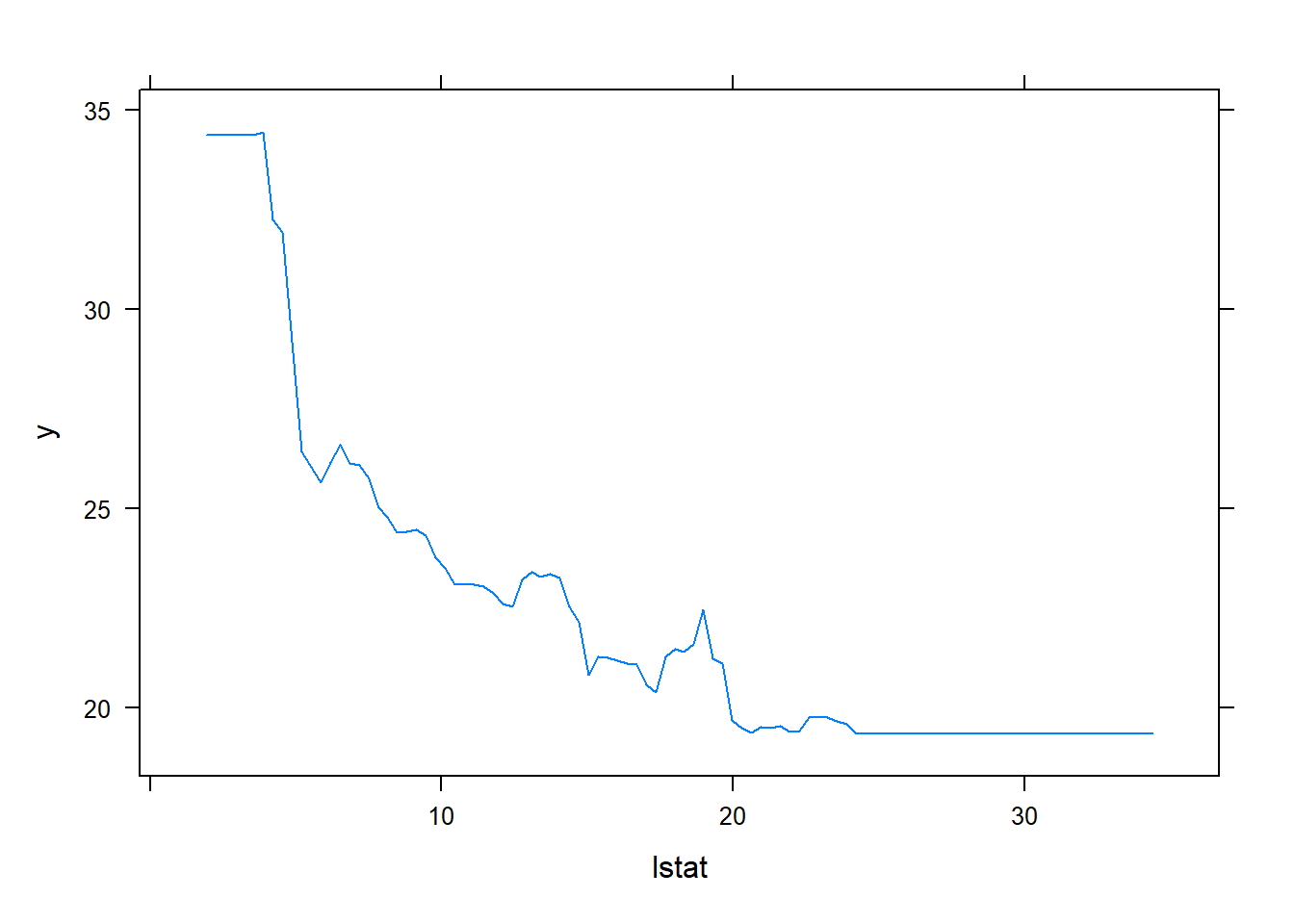

By plotting the partial dependence of rm and lstat on outcome variable, we see that

rm has a direct relation viz. more the number of rooms, higher the price increaseslstat has an inverse relation viz. higher the lower stata in the neighbourhood, lower the pricepar(mfrow = c(1,2))

plot(boost.boston, i = "rm")

plot(boost.boston, i = "lstat")

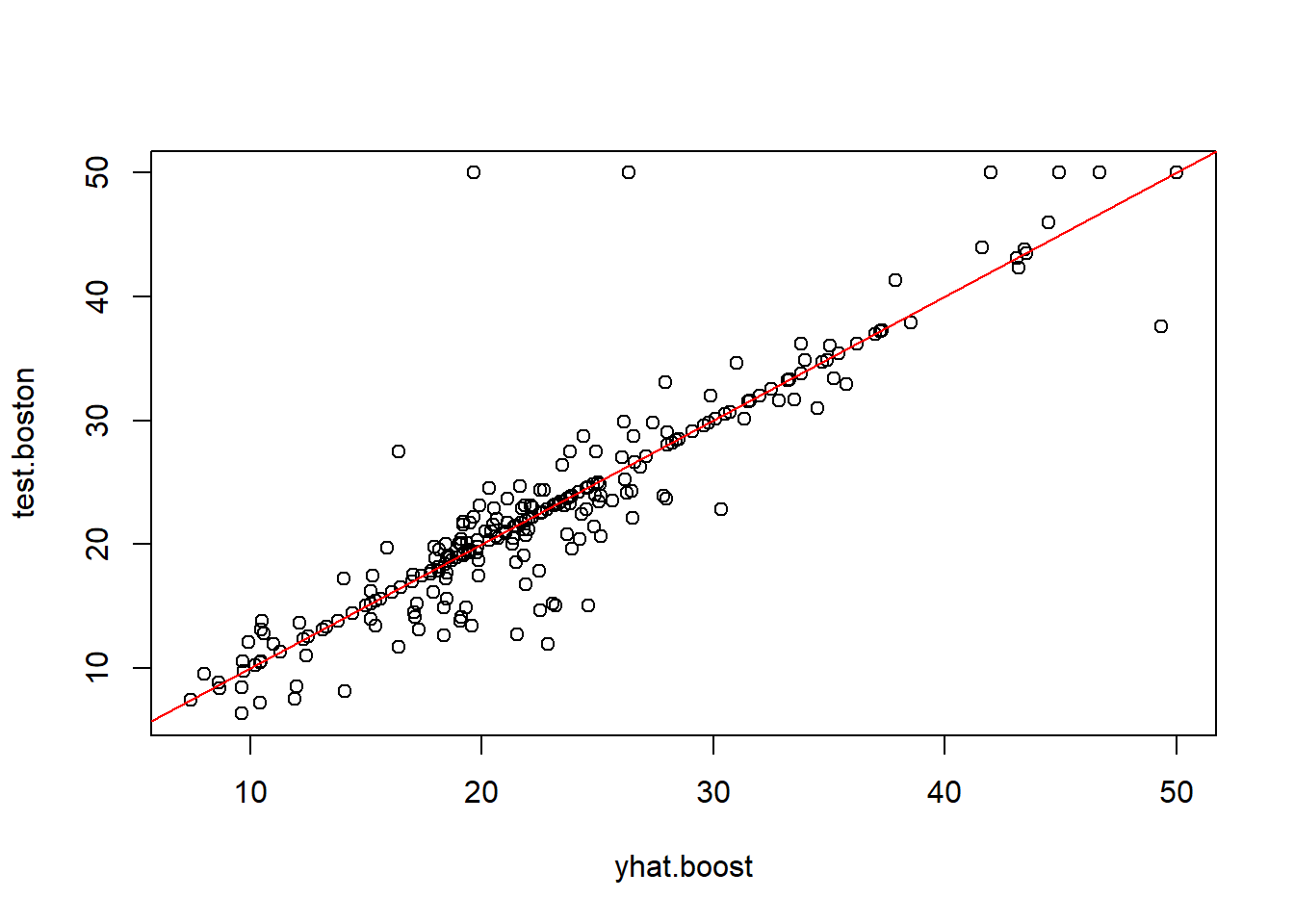

yhat.boost <- predict(boost.boston, newdata = Boston[-train.boston,],

n.trees = 5000)

#| fig-cap: "Predicted v/s Actuals for Boston test data using Boosted RF"

#| fig-cap-location: top

plot(yhat.boost, test.boston)

abline(0,1,col = "red")

Figure looks so much better. testing the accuracy now. starting with the MSE

mean((yhat.boost - test.boston)^2)[1] 12.98195Wow.. that’s significantly lower. How about the RMSE?

mean((yhat.boost - test.boston)^2)^0.5[1] 3.603047Amazing. This means our predicted value on an average is ±$3603 from the actual which is a signifcant improvement from the RMSE calculated by Random Forest ±$4480

Also referred as the shrinkage parameter, the default value is 0.001 but we will change this to 0.01

set.seed(1)

boost.boston2 <- gbm(medv ~ ., data = Boston[train,],

distribution = "gaussian",

n.trees = 5000,

interaction.depth = 4,

shrinkage = 0.01)

yhat.boost2 <- predict(boost.boston2, newdata = Boston[-train.boston,],

n.trees = 5000)The resulting MSE therefore is calculated as:

mean((yhat.boost2 - test.boston)^2)^0.5[1] 3.593472Now we’ve got it even lower at ±$3593

The function gbart() is used for regression analysis. This syntax slightly reminds me of the python syntax as we’re back to creating matrices for each test, train, x & y.

library(BART)

x_BART <- Boston[,1:12]

y_BART <- Boston[,"medv"]

xtrain_BART <- x_BART[train.boston, ]

ytrain_BART <- y_BART[train.boston]

xtest_BART <- x_BART[-train.boston, ]

ytest_BART <- y_BART[-train.boston]Creating the model now:

set.seed(1)

bart_model <- gbart(xtrain_BART, ytrain_BART, x.test = xtest_BART)*****Calling gbart: type=1

*****Data:

data:n,p,np: 253, 12, 253

y1,yn: 0.213439, -5.486561

x1,x[n*p]: 0.109590, 20.080000

xp1,xp[np*p]: 0.027310, 7.880000

*****Number of Trees: 200

*****Number of Cut Points: 100 ... 100

*****burn,nd,thin: 100,1000,1

*****Prior:beta,alpha,tau,nu,lambda,offset: 2,0.95,0.795495,3,3.71636,21.7866

*****sigma: 4.367914

*****w (weights): 1.000000 ... 1.000000

*****Dirichlet:sparse,theta,omega,a,b,rho,augment: 0,0,1,0.5,1,12,0

*****printevery: 100

MCMC

done 0 (out of 1100)

done 100 (out of 1100)

done 200 (out of 1100)

done 300 (out of 1100)

done 400 (out of 1100)

done 500 (out of 1100)

done 600 (out of 1100)

done 700 (out of 1100)

done 800 (out of 1100)

done 900 (out of 1100)

done 1000 (out of 1100)

time: 9s

trcnt,tecnt: 1000,1000Computing the test error MSE

yhat_bart <- bart_model$yhat.test.mean

mean((yhat_bart - test.boston)^2)[1] 15.94718uhoh.. it was 12.9 for the Boosted RF trees. So the RMSE can be calculated as:

mean((yhat_bart - test.boston)^2)^0.5[1] 3.993392That’s ±$3993 which is not as good as $3593 RMSE that the Boosted Tree with shrinkage gave us.

The calculations show that as per the RMSE, the accuracy of models can be ordered as:

Bagging < Random Forest < BART < Boosting < Boosting w/ Regularization